It is the key to ensuring that each transaction which reflects a debit will always have its corresponding entry on the credit side. It too provides a source of funding but is different from a liability because no repayment obligation exists. Retained earnings are all the profits made to date but unpaid to the owners in the form of dividends. Because profits are generated for the shareholders, retained earnings is theoretically due to the business owners. Financial analysis often involves both using or analyzing historic information and forecasting forward-looking financial statements. A thorough understanding of the engineering behind financial statements is essential for a valuation assignment or an M&A transaction.

Why You Can Trust Finance Strategists

Finance Strategists has an advertising relationship with some of the companies included on this website. We may earn a commission when you click on a link or make a purchase through the links on our site. All of our content is based on objective analysis, and the opinions are our own. The rights or claims to the properties are referred to as equities. In other words, all assets initially come from liabilities and owners’ contributions.

What is asset? Definition, Explanation, Types, Classification, Formula, and Measurement

- If you’re still unsure why the accounting equation just has to balance, the following example shows how the accounting equation remains in balance even after the effects of several transactions are accounted for.

- The accounting equation ensures that the balance sheet remains balanced.

- The inventory asset is recorded and the obligation to pay the suppliers is reflected as a liability.

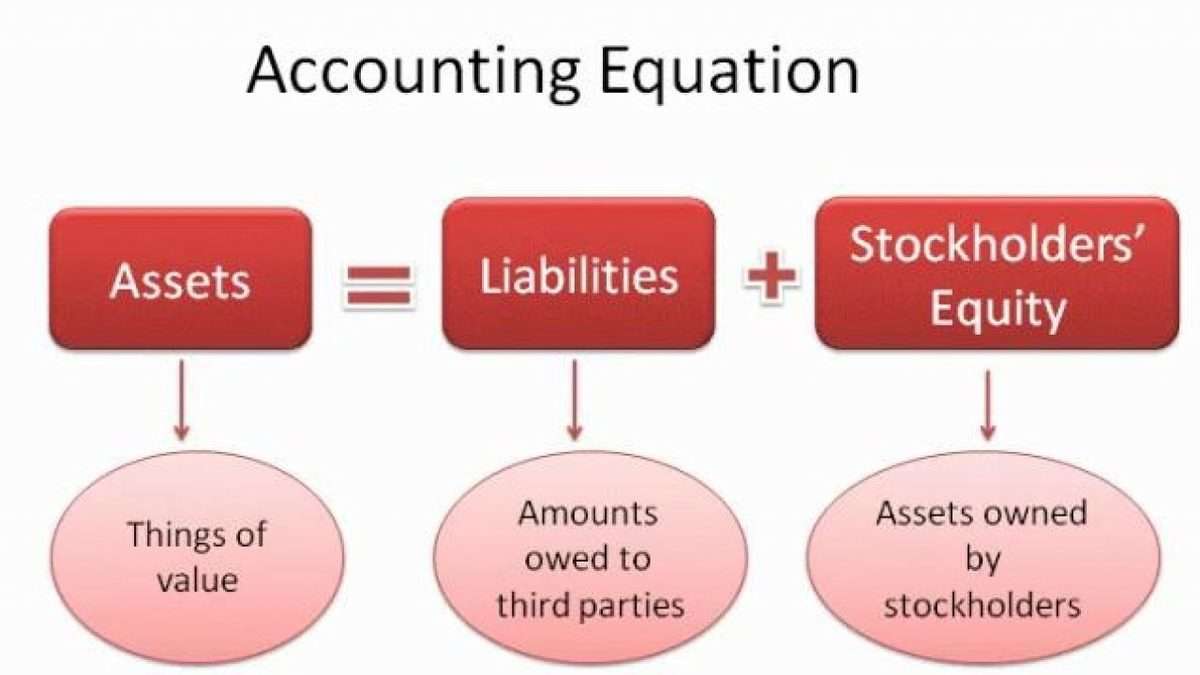

- It is fundamental to the double-entry bookkeeping system of accounting, which helps us understand from the illustration above that total assets should be equal to total liabilities.

- On 10 January, Sam Enterprises sells merchandise for $10,000 cash and earns a profit of $1,000.

- They are amalgamated and subsequently presented in form of a Balance Sheet that is simply a representation of the accounting equation in itself.

This formula represents the accounting identity, which must always be true for all entities regardless of their business activity. Finally, a cash flow statement can be produced for the period and reports the change in cash balances between periods. The inventory asset is recorded and the obligation to pay the suppliers is reflected as a liability. Net value refers to the umbrella term that a company can keep after paying off all liabilities, also known as its book value. It specifically highlights the amount of ownership that the business owner(s) has.

What Are the 3 Elements of the Accounting Equation?

The accounting equation is something that must be understood thoroughly by those who deal with money and those who want to ensure they are making the best decisions financially. The accounting equation matters because keeping track of each transaction’s corresponding entry on each side is essential for keeping records accurate. To illustrate how the accounting equation works, let us analyze the transactions of a fictitious corporation, First Shop, Inc. Equity includes any money that has been invested into the company by shareholders as well as retained earnings which have not yet been paid to shareholders as dividends.

What is your current financial priority?

Both liabilities and shareholders’ equity represent how the assets of a company are financed. If it’s financed through debt, it’ll show as a liability, but if it’s financed through issuing equity shares to investors, it’ll show in shareholders’ equity. The accounting equation is important because it allows the business or entity to correctly record transactions and, therefore, maintain their financial statements. However, an asset cannot be recorded because of the uncertainty of future benefits accruing from the salary expenditure. The balancing entry is a reduction in the equity of the shareholders. It is, in fact, an expense and all expenses reduce retained earnings which is part of the shareholder’s equity.

Components of the Basic Accounting Equation

The main premise of the balance sheet in this regard is to show the assets held by the company are equal to the sum of liabilities and equity held by the company at a particular date. While the accounting equation goes hand-in-hand with the balance sheet, it is also a fundamental aspect of the double-entry accounting system. To further illustrate the analysis of transactions and their effects on the basic accounting equation, we will analyze the activities of Metro Courier, Inc., a fictitious corporation. Refer to the chart of accounts illustrated in the previous section.

The accounting equation will always balance because the dual aspect of accounting for income and expenses will result in equal increases or decreases to assets or liabilities. Because it considers assets, liabilities, and equity (also known as shareholders’ equity or owner’s equity), this basic accounting equation is the basis of a business’s balance sheet. The purpose of this article is to consider the fundamentals of the accounting equation and to demonstrate how it works when applied to various transactions. The balance sheet is the linchpin of the structural integrity of the three key financial statements. It must always balance and the fundamental accounting equation, assets equals liabilities plus equity, provides the basis for the recording of all business transactions.

For example, you can talk about a time you balanced the books for a friend or family member’s small business. The accounting equation will always remain in balance if the double entry system of accounting is followed accurately. The above accounting equation format provides the management and the stakeholders a clear snapshot of the asset, liability and equity position at a particular point of time.

The accounting equation is similar to the format of the balance sheet. The accountants should ensure that the concept of accounting equation and its rules are properly followed and the transactions are daily and accurately recorded. The combined balance of liabilities and capital is also at $50,000. If your accounting software is rounding to the nearest dollar or thousand dollars, the rounding function may result in a presentation that appears to be unbalanced. This is merely a rounding issue – there is not actually a flaw in the underlying accounting equation.

For example, if a business signs up for accounting software, it will automatically default to double-entry. Metro Courier, Inc., was organized as a corporation on January 1, the company issued shares (10,000 shares at $3 each) of common stock for $30,000 cash to Ron Chaney, his wife, and their son. However, equity can also be thought of the accounting equation is defined as: as investments into the company either by founders, owners, public shareholders, or by customers buying products leading to higher revenue. The equations has certain rules that every company should follow. They give us guidelines regarding how to do accounting equation. On 28 January, merchandise costing $5,500 are destroyed by fire.

If assets increase, either liabilities or owner’s equity must increase to balance out the equation. The shareholders’ equity number is a company’s total assets minus its total liabilities. Whether you call it the accounting equation, the accounting formula, the balance sheet equation, the fundamental accounting equation, or the basic accounting equation, they all mean the same thing.

Notice: Trying to access array offset on value of type bool in /home/ccva/domains/ccva.com.ar/public_html/wp-content/themes/flatsome/inc/shortcodes/share_follow.php on line 29